The resulting impact on debt mutual funds’ risk appetite had raised concerns about how NBFCs will meet their funding needs

Mutual funds pared stake in most non-banking and housing finance companies or NBFCs in September as defaults in repayment by group companies of Infrastructure Leasing & Financial Services (IL&FS) and subsequent ratings downgrades led to fears of a contagion in the sector.

Mounting concerns over asset-liability mismatches at NBFCs have prompted fund houses to prune stake in these companies.

Fund houses largely offloaded stake in Shriram Transport Finance Co, Indiabulls Housing Finance, Dewan Housing Finance Corp, L&T Finance Holdings, and Reliance Capital, as per the data compiled by ICICIdirect.com and East India Securities.

“Most fund houses have sold shares of these companies as they largely fund long-term loans in their portfolio through short-term borrowings which sparked concern of a liquidity gridlock due to asset liability mismatch,” said a fund manager on condition of anonymity.

“Besides, cost of raising funds through debt shot up during the month because of rising interest rates and weak sentiment for the sector,” he added.

Further, anticipating an increase in the cost of borrowing, analysts downgraded earnings estimates for non-bank lenders because they expect net interest margins to take a hit.

Shares of Shriram Transport Finance Co, Indiabulls Housing Finance, Dewan Housing Finance Corp, L&T Finance Holdings and Reliance Capital fell 14-59 percent in September.

According to Credit Suisse report, in the three years, local funds emerged as the second biggest provider of liquidity to NBFCs, and their exposure to commercial paper rose three times in the same period.

Mutual fund industry held nearly 60 percent of total NBFC issuance.

NBFC debt—including commercial paper and bonds accounts for almost 28 percent of the total mutual fund corporate debt exposure.

The share of corporate debt in the total debt of local mutual funds rose to 67 percent in July 2018, compared with 33% in the last four mar ..

What led to increased exposure of mutual funds to NBFCs?

Under immense pressure to shore up their total funds under management in order to stay ahead in the league tables, AMCs have been growing their debt and liquid funds. Though AMCs earn very low fees from these schemes (especially on liquid schemes), they are able to garner vast amounts from institutional investors.

Debt funding by MFs to NBFCs stood around Rs 2,30,000 crore as at March-end. It more than doubled between September last year and March. While the exposure to NBFC papers as percentage of debt AUM of MFs works out to around 18 percent, the same will be much more if we exclude government securities.

Crisis in NBFCs?

While higher interest rates were anticipated in FY19, NBFCs were caught completely off guard on the shrinking and in some cases complete withdrawal of liquidity triggered by defaults by group companies of Infrastructure Leasing & Financial Services (IL&FS).

The resulting impact on debt mutual funds’ risk appetite had raised concerns about how NBFCs will meet their funding needs.

As recent as April, debt schemes of mutual funds gorged on NBFC papers. Now, they seem to have limited appetite and can no longer digest issuances by NBFCs.

Bulk growth fuelled by MFs

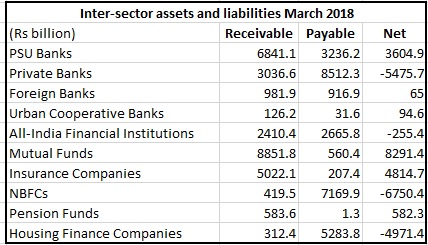

According to RBI’s recent Financial Stability Report, Mutual Funds were the dominant fund providers in the system, followed by the insurance companies, while NBFCs followed by scheduled commercial banks were the dominant receivers of funds.

Source:RBI

Housing finance companies (HFCs) were the second largest borrowers of funds from the financial system, with gross payables around Rs 5,28,400 crore as at FY18-end.

The borrowing pattern of HFCs was quite similar to that of NBFCs, except that MFs contribution to HFCs gross borrowings was higher at 32 percent.

What next?

A lot will change in the aftermath of the IL&FS crisis. Mutual funds as a source of funding will clearly take a back seat. Following the default of IL&FS and group companies, mutual funds will limit lending to the quality names among NBFCs. There could be pressure from investors as well, to reduce exposure to NBFCs.

Secondly, large institutional investors which invests in liquid schemes of mutual funds may not be comfortable with mark to market losses (as underlying papers get marked down) and prefer safer avenues in bank deposits.